Workers’ compensation insurance – or workers’ comp – protects people who get injured at work. It also protects businesses from potential legal issues. Workers’ comp typically covers costs like lost wages, medical expenses, and similar. Specific laws vary between U.S. states, so make sure you understand which ones apply to your business. This type of insurance is highly regulated, and without the right tools, it can be a major headache for HR.

What is a Workers’ Compensation Audit?

Workers’ comp audits happen annually, whenever your policy term expires. They’re not a sign that your business has done anything wrong. Audits can be time-consuming, but with the right preparation, they won’t result in fees or other penalties.

A workers’ compensation audit is a systematic review of your records, to ensure you’ve paid the right amount over the past year. Your insurance carrier will go over your premium payments and compare them to the estimates you provided at the start of the policy period. The goal is to ensure that your payments accurately reflect your payroll costs and your level of risk.

Depending on your location, your budget, and the size of your business, you may have a few options for workers’ comp insurance carriers. In most states, private insurance companies are the norm. In some areas, businesses can also access state funds for workers’ comp. Larger companies can also choose to self-insure.

What Happens During a Compensation Audit?

During a workers’ comp audit, HR works closely with the company’s insurance carrier. You’ll review your payroll and other expenses in detail and compare them to your original estimates. There are several reasons your projected numbers could have changed throughout the year:

- Rapid business growth and hiring

- Unplanned layoffs

- Voluntary turnover

- Misclassification of employees and their risk levels

- Clerical errors, including failure to include deductions

Need more information about Workers’ Compensation? Get our FREE guide here: What Employers Need to Know about Workers Compensation.

Depending on your insurer, your audit might take place by phone, online, or in person. Because they’ll need to review sensitive financial documents, make sure you have a secure way to share information.

Documenting Workers’ Compensation

The exact type of documentation you’ll need depends on your location, insurer, industry, and business size. You should find out what you need when you first open your insurance policy – make sure to confirm with the carrier and double-check your local laws. That might seem like an extra step, but it’s the best way to ensure you’ll be prepared for your next audit.

Most workers’ comp audits include a review of:

- Financial records, such as the business’s P&L

- Payroll reports and records

- Tax forms such as W-2s, 1099s, Form 941, and Form 944

- Federal tax returns

- Certificates of insurance for every subcontractor

- Detailed descriptions of each business function, including each employee’s risk level at work

The Results of a Worker’s Comp Audit

At the end of a workers’ comp audit, you’ll receive an audit report. Usually, it will include one of two results. You might have an audit variance, meaning you owe more than you already paid. In that case, you’ll have to pay an additional premium to cover the difference. On the other hand, if you overpaid during the year, you’ll receive a refund.

Make sure to review the complete report in detail. If you disagree with the auditor’s findings, contact your insurer immediately. They can instruct you on how to file a formal dispute.

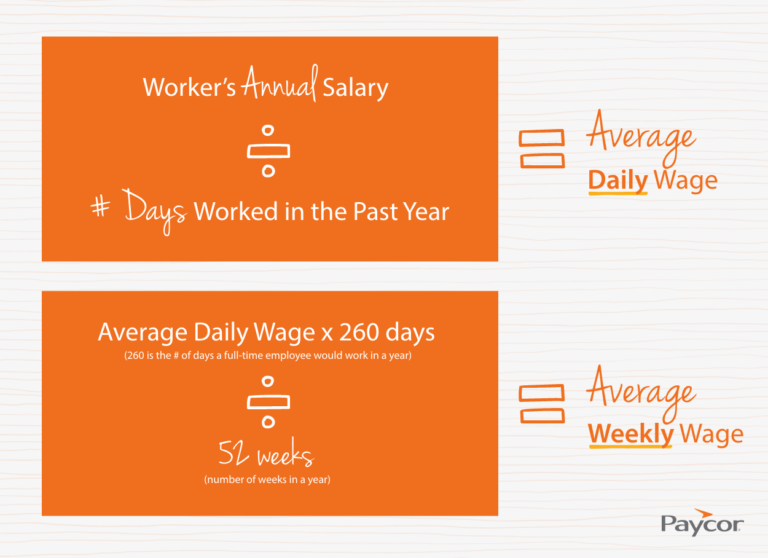

Calculating Workers’ Comp

Like most other compliance issues, calculating workers’ comp is different between U.S. states. In most states, it’s based on the worker’s average weekly wage, or AWW. Here’s how you calculate AWW:

Workers’ comp payments are generally higher for more severe injuries. Each state has a maximum weekly rate for payouts.

When it comes to calculating your insurance premium, your insurer will consider:

- What type of work your employees perform

- How many employees you have

- Your average weekly payroll

- Your company’s history of claims

- Other state regulations

How Paycor Helps

Paycor is purpose-built to help with workers’ comp. Our pay-as-you-go workers’ compensation solution allows you to automate insurance payments based on payroll. With our tools, business leaders can eliminate large down payments and avoid end-of-year surprises. We can even help you find the top-rated insurance carriers to keep you and your team covered.